What Could Possibly Go Wrong?

What’s the highest interest rate that you have ever found yourself paying on a credit card or for a loan? For those of us unfortunate enough to carry a credit card balance, maybe things got as bad as 15% or even an outrageous 20%?!? For us, I think the highest interest rate we have ever accepted was something around 5%, and that was an auto loan on a used car just to help build up our credit history… Read on to find out what loan offer I recently got in the mail. It really starts to make you wonder!

What Could Possibly Go Wrong?

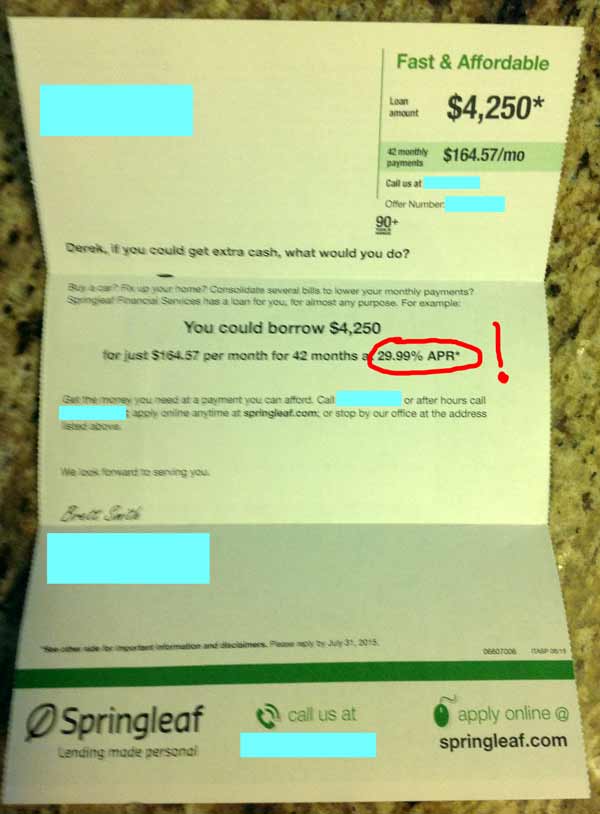

See the fun picture below where I was recently offered a loan at a whopping 29.99% annual percentage rate. They just had to add in that last 0.09% in there, didn’t they? Who in God’s name would actually go through and sign up for one of these shit loans? I assume there must be someone out there dumb enough or desperate enough to fall for this, or the company wouldn’t still operating a business. But then again, I am questioning how smart this company is because our credit scores are both above 800… Somehow I don’t think we are Springleaf’s target market…

30 Percent APR Loan!

What’s the Harm in Taking a 30% APR Loan?

But you could have $4,250 today to buy that new TV or what-have-you! Why not take the loan today and worry about the consequences tomorrow. Well, just for fun I put together this neat little chart to show you just how badly Springleaf would be screwing me over if I decided to take this offering.

Springleaf Loan

That’s right – if I took the Springleaf loan today versus investing my money, I would end up more than $10,332 in the hole at the end of three and a half years (42 months)! Yes, I wouldn’t have that shiny new used car, or that 80″ TV, but I would have $10 grand in my pocket!

Thinking for the Long Run

If you are here reading this, then you would probably never take out a loan under such outrageous conditions. What could possibly go wrong? Unless you have $10,332 to lose, then everything!

I realize that I’m preaching to the choir a bit here – but come on people! If more folks would learn to control their short-term desires and focus on the long-term, we would be so much better off as a species. That goes for just about everything: education, the environment, and yes finances!

Nothing can go wrong, except become part of statistics for people ripped by credit companies.

Cheryll Abanto recently posted…Stock Splits: How You Can Benefit As An Investor

LOL – so true Cheryll!