Stock Market Investing with IRAs – Traditional and Roth

Tax advantaged retirement accounts are almost always better than just investing your money in your own personal investment account. This is because you are getting a large bonus by avoiding the payment of taxes at some point in the process – either before your money is invested or at withdrawal of your money. This investing post will discuss IRAs and how they can be a great tool to help you save for retirement.

What is an IRA?

Individual Retirement Accounts (IRAs) are another type of retirement account that share some similarities with the 401(k) plan. These programs let you invest in the stock market to save for your retirement. There are many types of IRAs, and some of the more elaborate versions are outside the scope of this post. The two main types of IRAs that are the most used are the Traditional IRA and the Roth IRA.

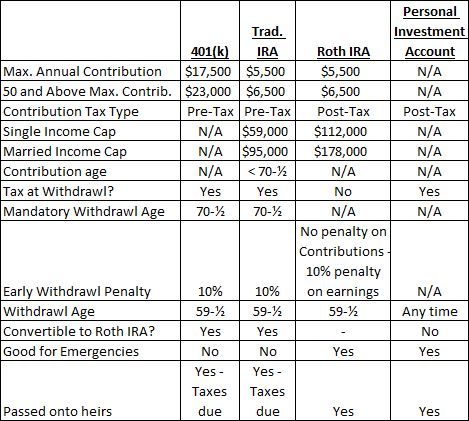

Because Traditional IRAs and Roth IRAs are similar to 401(k) plans and each other in concept, a table that compares the similarities and differences will be the most helpful way for me to show you how each one works. Each of these types of retirement accounts has just enough of a difference between them to make things a bit confusing if not compared side-by-side. The figure below illustrates the similarities and differences among a 401(k), Traditional IRA, Roth IRA, and a personal investment account.

IRA Comparison Table – All values based on 2014 Guidelines

Picking the Right IRA for You

If you are ready to begin investing in an IRA because of its great income tax benefits, you need to make sure you pick the type that is right for you. As you can see from the figure above, there are several important differences to be aware of between these two different types of IRAs. Generally, investors prefer to use pre-tax money whenever possible because it grows at a faster rate due to compounding interest. When tax is eventually taken out at withdrawal, you will end up farther ahead by using pre-tax investments.

One problem with IRAs is the maximum income caps on traditional IRAs and Roth IRAs. How do the income caps affect you and indicate investment programs available to you?

IRAs and Income Caps

The income cap values shown in the figure above are established for 2014, and these values will generally increase each year. If you are on the borderline, it will pay to double check your status.

If you do not qualify for a traditional IRA because your income is over the cap, that is OK. You may still qualify for a Roth IRA. A Roth IRA forces you to use after-tax money to invest, but when you eventually withdraw the money at retirement age you will not have to pay any income tax on the earnings. That’s right – no tax :-)!

Bonus Roth IRA Feature

One other great feature of a Roth IRA is that if you need to withdraw some money for an emergency, you can withdraw your contributions (not earnings) without any type of penalty. The same cannot be said for the 401(k) or the traditional IRA – these retirement accounts will hit you with a 10% penalty in addition to the income tax you will be required to pay on the total withdrawal!

I love this feature of the Roth IRA. Because you can withdraw your contributions without penalty, you can almost treat your Roth IRA as an emergency fund. Obviously, you do not want to tap into this money often (if at all). But, it provides extra sense of security if something serious does happen. The option exists to access your finds without paying a huge tax penalty. I love the feeling that I will always be able to get at the money if something really serious ever comes up.

Stock Market Investing with IRAs – Traditional and Roth – Final Thoughts

It’s never too late, or early, to get started investing in the Stock Market. If you are ready to learn more about stock market investing, check out my free 150+ page eBook – Stock Market Investing for Newbies. If you don’t have an IRA currently, please consider signing up for one today!