The Best Way to Invest In The Stock Market

If the company that you work for has a 401(k) plan, then you should be investing in the stock market! If you run your own business, then you should be investing in the stock market by starting your own 401(k) plan! If your company does not have a 401(k) plan, complain to whomever will listen that you need one right now!

What is a 401(k) Plan?

I am glad that you asked! Basically, a 401(k) plan allows you to invest pre-tax money in the stock market that can be used for retirement. Typically, companies will match the contribution that you set aside (sometimes even dollar for dollar up to a set percentage). The current annual contribution limit is $17,500 (2014). Your stock market investments will grow tax free until you begin to withdraw the money at retirement age. You can withdraw from your 401(k) at any time, but there is a 10% penalty on any withdrawals made before the age of 59-½.

What are the Benefits of a 401(k) Plan?

In the case that you do not realize all of the benefits of this type of retirement savings plan, let me fill you in on why 401(k)s are so great for you and me:

- 401(k)s reduce your annual taxable income. This means you pay less money to the IRS and keep more for yourself. If you are able to contribute the annual maximum (currently $18,000), you are saving nearly $4,400 a year on taxes! With that kind of extra money, you could easily start your own side business or pay off your debt.

- Because your money is invested pre-tax, compound interest kicks into high-gear on this untaxed amount that is invested. When you withdraw the money down the road, you’ll come out way ahead by using pre-tax money to investment.

- Most companies have an employer match – this means you are getting free money to invest in the stock market. Just to make the math simple, say you make $100,000 a year. If you contribute 10% of your income, that’s $10,000 a year. If your company matches contributions up to 5%, you are receiving a free $5,000 to invest in the stock market each and every year!

- If you are self-employed, you can contribute up to $53,000 a year into your own solo-401(k) – all with pre-tax dollars!

- 401(k)s come with flexibility in how to handle the money if you die and your spouse is still alive. The details are beyond the scope of this post, but there are a number of flexible options your spouse can take to maximize the amount of money that they will receive when they need it.

What Are the Catches of a 401(k) Plan?

Now, all of these awesome features that 401(k)s have come with some catches. Be aware of three rules for 401(k)s:

- When you decide to withdraw the money from a 401(k), you have to pay ordinary income taxes on it.

- You cannot withdraw the money from a 401(k) until age 59-½ without a incurring a hefty 10% penalty. This is in addition to the ordinary income tax that you would pay outlined in bullet #1 above.

- When you turn 70-½, you are required to initiate minimum withdrawals from your 401(k) account. The withdrawal rate is designed to reduce your 401(k) to zero prior to your death.

401(k) Plans and Debt Payoff

But Derek – what if I have a boatload of consumer debt? Should I still contribute to my 401(k)? Or, should I focus on paying down my debt?

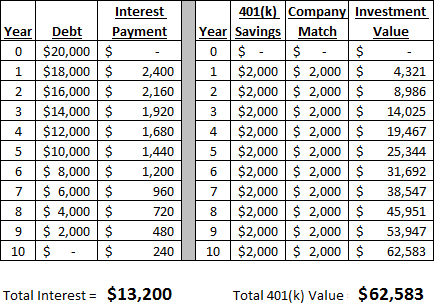

Let’s look at a quick example to answer the question you asked. The figure below shows a scenario where Poor Peter has $20,000 of credit card debt. For whatever reason, he cannot transfer his balance and he’s stuck paying 12% APR interest on the debt. We’ll assume that Poor Peter makes $45,000 a year, and the average stock market investment annual return is 8%.

Debt vs. 401(k) – Cage Match!

What should Poor Peter do in a situation like this?

You may think that since the credit card debt has a higher interest rate than what Poor Peter can get from the stock market (12% vs. 8%), it would be better for Poor Peter to pay off the debt. Let’s find out if this is the best strategy.

Let’s say that the best Poor Peter can do is save $2,000 a year. This means that it would take him 10 years to pay off all of his debt at 12% APR. At the end of this scenario, Poor Peter would have paid $13,200 in interest. Ouch!

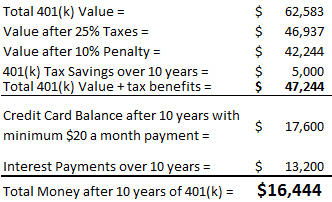

Instead, let’s assume that Peter pays the absolute bare amount on his credit card debt (say $20 a month) and invests in his company’s 401(k) plan instead. At the end of 10 years, Poor Peter has $62,583 in his 401(k)! He could theoretically withdraw all of the money from his 401(k) (this is a horrible idea, but I am just using it for illustrative purposes), pay the 10% early withdrawal penalty on it, pay off the credit card debt, and still be ahead by more than $16,000! The figure below shows the math on this scenario just to illustrate how this would work:

401(k) Wins!

401(k) and the Company Match

Why would Poor Peter come out so far ahead by contributing to his 401(k) instead of focusing on the credit card debt?

It is because of the company match! Poor Peter would be leaving $2,000 on the table each year by not participating in this company’s 401(k)!

In addition, by putting $2,000 into the plan each year, Poor Peter is paying $500 less in federal income taxes each year (assuming he is in the 25% tax bracket) because the 401(k) contributions reduce Poor Peter’s taxable income. For this example, the credit card APR on the debt would need to be nearly 27% before Poor Peter would be better off to focus on the credit card debt first.

Let me repeat this point just in case you were spacing out for a second. Unless you have consumer debt with APRs > 25%, it is almost always better to contribute to your 401(k) up to your employer match!

401(k) and Pre-Tax Investing vs. Post-Tax Investing

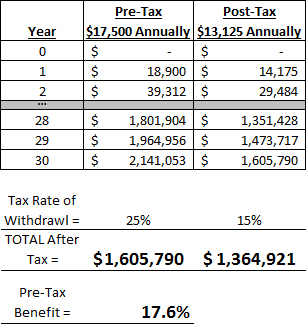

One last benefit of the 401(k) that I would like to illustrate is the power of investing with pre-tax money versus post-tax money. The figure below shows two different investment examples with an 8% annual return. Scenario number one assumes that we have $17,500 a year of pre-tax money to invest. If we use our 401(k) as a pre-tax investment vehicle, the account will grow to $2,141,053 after 30 years (not counting company match).

For scenario number two, what if we decide that the 401(k) is not for us and we invest the money in our own personal investment account. This would be like investing $13,125 each year ($17,500 pre-tax, minus 25% taxes, equals $13,125). At the end of 30 years, our personal investment account will grow to $1,605,790.

Pre-Tax versus Post-Tax Investing

As you can see in figure above, I have made assumptions around the tax rate at withdrawal. For scenario number one, the pre-tax investments will count as normal income and will be subject to a 25% income tax rate. Under scenario number two, we already paid taxes on the money before the investments were purchased, so we will be subject to the lower 15% long term capital gains tax rate.

Because of the power of compound interest, the pre-tax account actually grew to be nearly 18% larger than the post-tax personal investment account. This is the incredible power of using pre-tax investment money. This is why the 401(k) is such an awesome vehicle for building wealth by investing in the stock market!

The Best Way to Invest In The Stock Market – Final Thoughts

Now that we have probed the depths of the 401(k) plan, I hope you will agree that you would be brain-dead not to contribute to your 401(k) at least up to your employer match. If you are not doing this, then you are leaving huge overflowing bags of freshly minted money on the table! If your company does not currently offer a 401(k), then close your browsing window and contact your HR department immediately. I will be waiting here for you to take care of that…

It’s never too late, or early, to get started investing in the Stock Market. If you are ready to learn more about stock market investing, check out my free 150+ page eBook – Stock Market Investing for Newbies.